What is Letter of Credit? – The Basics Explained

The following video, explains the basics of a credit letter, also known as a documentary letter of credit (or LoC), which is a financial guarantee from a bank ensuring timely payment from a buyer to a seller in international transactions and important points to be aware of if you intend to use one as a method of payment.

In this video, the following points are discussed:

- The Definition of a Letter of Credit

- Why Trade Under a Letter of Credit?

- Types of Letters of Credit

- A Way To Make Money Without Money?

- The Rules of UCP600

Knowing how to use an LoC is an important method of payment as it’s a very versatile instrument and when used correctly, a very import method of payment to have in your trade finance arsenal, helping both the buyer and seller and can importantly, ensure that you get paid.

- Defining a Letter of Credit

- How Does a Letter of Credit Work?

- The Different Types of Letters of Credit

- Letter of Credit Costs

- Applying for an Letter of Credit

- Advantages of an Letter of Credit

- Disadvantages of an Letter of Credit

- Managing Risk with an Letter of Credit

- UPC 600 – The Rules of the Game

- A Letter of Credit Example

Letter of Credit Definition:

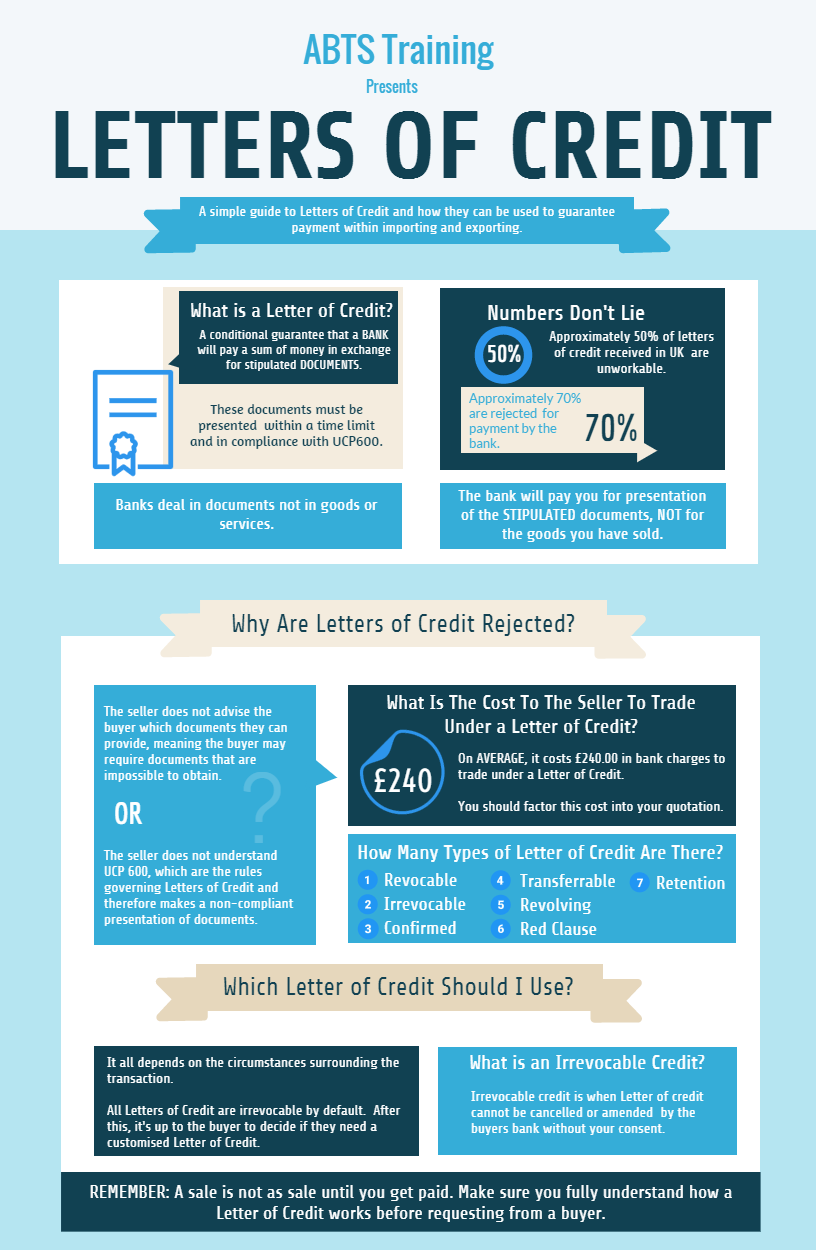

With a letter of credit the issuing bank or financial institution, guarantees payment to the seller within a time frame and for a stipulated amount. Payment to the seller is contingent upon the fulfillment of conditions outlined in the LoC. The buyer themselves does not pay the seller but it’s the buyer’s bank providing payment on a complying presentation by the seller of the stipulated documents.

In addition to this, an LoC can allow the seller to receive funds before the goods are delivered, which can be advantageous if capital is needed up front and avoids payment delays.

In short, it’s payment security for the seller and they can ship goods knowing that the payment commitments of the buyer will be met.

A letter of credit is not “credit” like credit enables you to borrow on a credit card. It is not a credit facility. A buyer will have to make immediate payment to their bank or have the debt secured in the form of a loan to open a letter of credit.

How Does a Letter of Credit Work?

A letter of credit, is a conditional guarantee to the seller to receive payment from a bank or financial institution. Being paid by an LoC as a seller is advantageous because it provides security to you. You don’t need to worry about the state of your buyers business as the bank makes direct payment to you.

Once you receive the letter of credit, you can ship goods to the buyer without worrying about the buyers cash flow, available funds or if they were to even go bankrupt and close their doors. You would still be paid which helps a business managing risk.

For sellers, this can be very beneficial for new customers giving you large orders as it reduces the risk of non payment because the bank pays you making international trade transactions effectively much less risky for sellers.

However, the most important point that I can’t stress enough is that an LoC is a conditional bank guarantee, that on correct presentation of the STIPULATED documents required, as the seller, you’ll be paid.

In other words, it’s incredibly important to understand that the documents presented comply with the conditions of the LoC. What this means in simple speak, is that you will have to present to the buyer’s bank the stipulated documents specified in the letter of credit in order to be paid.

The buyer’s bank undertakes the financial commitments to ensure the beneficiary’s demand of payment upon meeting the specified conditions, thereby providing assurance and more security for both parties involved in the transaction.

The issuing bank not does care and has no interest in the goods themselves. They don’t care if the goods were received by the buyer, they don’t care what the goods are, they don’t care if the goods sank on the vessel on the way to the port of destination. They only care that the documents presented comply with the stipulated documents in the LoC.

Once they are correctly presented, the importer’s bank will issue the buyer’s payment to you, the seller and its contractual obligations are completed.

An important point to note is that most letters of credit (i.e. 70% – the vast majority) are unpaid on first presentation so it’s vital that you understand how they work if you’re going to start trading using one.

How to Open a Letter of Credit

The workings of an LoC is a complicated process and not something that I would ever recommend to anyone that doesn’t have a very good understanding of the process. With that in mind, this blog is not intended to be a detailed guide on how they work but more of an overview.

So lets look at this from the perspective of the seller. A potential buyer contacts you and asks you to quote for 100 widgets which you oblige and send back your quotation or proforma invoice with your terms of payment as a letter of credit with instructions on how the LoC should be setup. Both parties agree letters of credit terms and required documentation.

The order is accepted at which point, the buyer should contact you to discuss the details of the letter of credit and to make sure that the LoC is workable for you. The buyer will have to state what documents they want to be presented for payment which you as the seller must make sure you can provide.

This in itself is very involved and beyond the scope of this introduction but what needs to be understood is that the buyer will require those documents to clear the goods through customs once they arrive at the port of destination. What those documents are will depend on various factors and we won’t go into any more detail on that here.

So the buyer will state what documents they require in order to clear the goods through customs which should be agreed with the seller beforehand and once agreed, they will go to their bank and ask to open a letter of credit.

The buyer will have to prove the source of funds (the buyer has the payment obligation) or arrange a loan from the bank and the letter of credit is opened with the agreed STIPULATED DOCUMENTS to be presented by the seller for payment.

Beware the SCAMMERS!!

A letter of credit should never be received directly from a buyer but should only ever be received by a nominated bank which the seller will nominate (the exporter’s bank), usually their own bank where the company bank account will be.

If a letter of credit is ever received directly from a buyer, it’s a fraud and never ship the goods!

It’s a SCAM!

Receiving the Letter of Credit

Once the exporter’s bank receives the LoC from the issuing bank, the seller will be notified and they can prepare the order and get the goods shipped. The bank guaranteeing the letter of credit provides assurance of payment to the seller, the buyer will fulfill their financial obligations.

The widgets sail off on the vessel headed for the buyer’s warehouse at which point the seller must organise the STIPULATED DOCUMENTS for presentation to the bank.

Stipulated Documents

The process of organising and ensuring that the stipulated documents are correct on first presentation is a subject on it’s own and not something that can be covered in this introduction.

This should not be underestimated and ideally only trained professionals would work with letters of credit.

Again I would like to point out that most letters of credit (70%) go unpaid on first presentation so it’s essential to know exactly what the stipulated documents are and present them in the correct format and avoid any legal risks.

This is covered in our online Letter of Credit course and again, please consider enrolling if you’re going to be dealing with letters of credit.

For this introduction, we will assume that the seller has all the stipulated documents and that they are in good order, everything is correct and they confirm to UCP 600 (see below for more on UCP 600).

The stipulated documents are presented to the bank and approved at which point the bank pays, the funds are released to the seller and the documents are forwarded on to the buyer so they can clear the goods through customs.

Beware – letters of credit have an expiry date so you must be aware that you have to complete the process and provide the stipulated documents by the deadline in order to receive payment from the financial institution or buyer’s bank. As long as you submit before the existing letter of credit deadline, you’ll have nothing to worry about and the bank will pay you.

This is a very basic overview or what a letter of credit is and how it works but please don’t be lulled into a false sense of security that they are easy to work with.

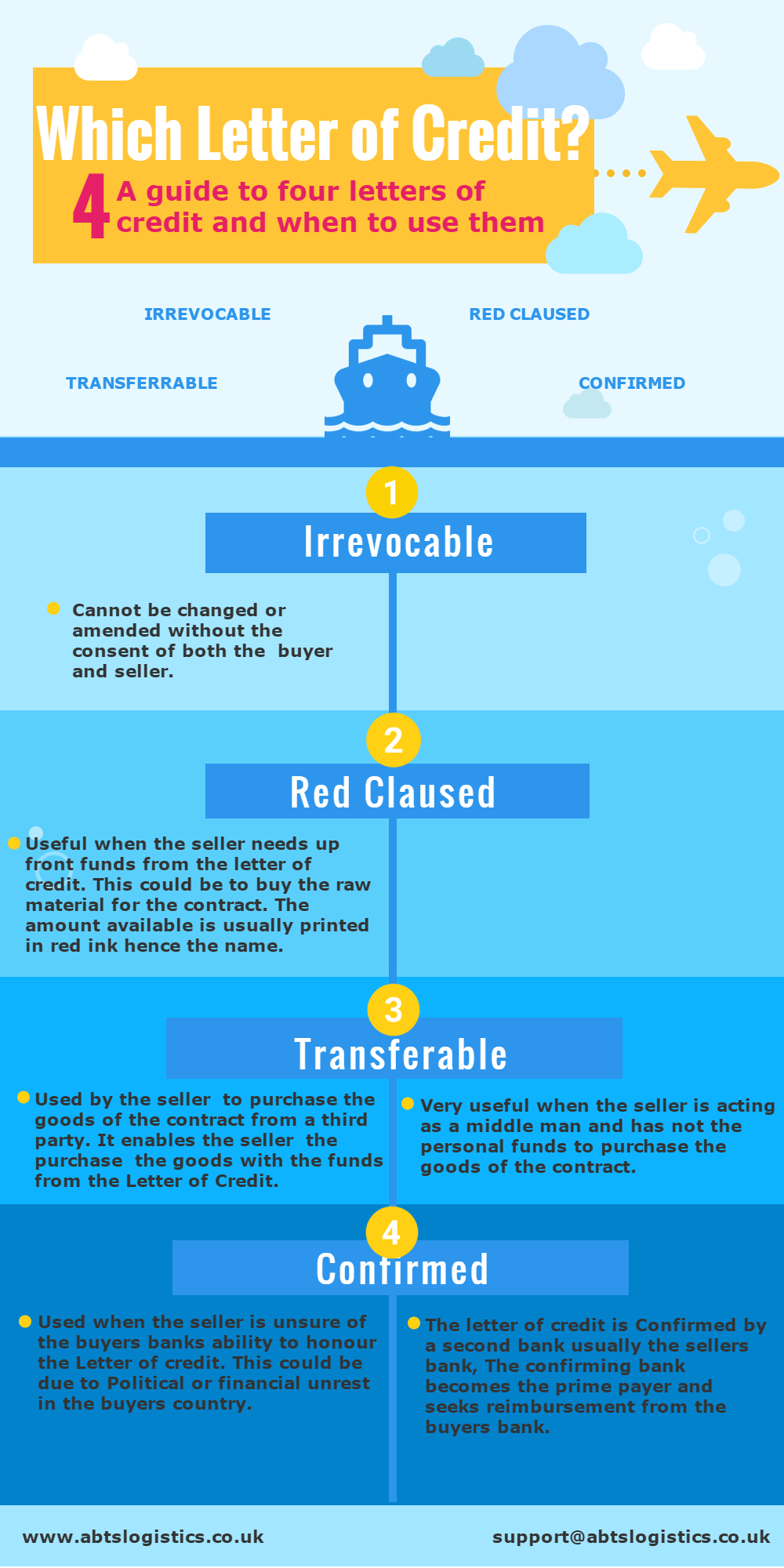

Types of Letters Of Credit

There are several types of letters of credit so lets start with the four most common types and when to use letters of credit as trade finance options.

Commercial letters of credit are a widely used financial instrument where a bank directly pays the seller, distinguishing them from other types of letters of credit.

IRREVOCABLE CREDIT

Irrevocable letters of credit, once it’s born, cannot be changed or amended without the consent of both the buyer and seller.

RED CLAUSED

This clause is very useful when the seller needs to raise funds from the letter of credit, for example to buy raw material for a building contract. The amount available is usually printed on the letter of credit in red ink, hence the name “red claused”.

TRANSFERABLE

This type of LoC can used by the seller to purchase goods needed to fulfill the contract from a third party. For example, steel, concrete and brinks to complete a building contract. This is extremely useful when the seller may not have available funds to purchase the goods to complete the contract, so could use this method to raise those funds by guaranteeing payment to the third party supplier.

CONFIRMED LETTER OF CREDIT

These letters of credit are used when the seller is unsure of the buyers’ bank’s ability to honour the letter of credit perhaps due to political or financial unrest or differing laws in the buyers country. The exporter’s bank reviews the seller’s bank and the letter of credit is confirmed by a second bank (the confirming bank) which is usually the seller’s bank.

The confirming bank becomes the prime payer and seeks reimbursement from the buyer’s bank. A documentary credit serves as a payment mechanism that involves a bank providing an economic guarantee to the exporter, ensuring payment upon fulfillment of certain documentation requirements.

A confirmed letter of credit is complicated and should be understood before attempting to use one.

To embed this infographic, copy and paste the code below:

Letter of Credit Costs

When using an LoC as a trade finance solution you need to consider the credit costs. These costs can vary depending on the issuing bank, the size of the letter of credit and the type of LoC. Banks charge a fee for issuing a letter of credit which is often a percentage of the amount being backed. For example a bank may charge 0.75% of the amount.

In addition to the issuance fee there may be other costs such as a commitment fee, fronting fee or negotiation fee. These additional fees can add up so you need to factor them into your trade finance strategy.

Exporters and importers should talk to their bank as well as other banks to get a clear understanding of all the fees and negotiate the best terms. By doing so you can make sure the benefits of using a letter of credit outweigh the costs and it becomes a viable option for your international trade.

Applying for a Letter of Credit

Applying for a letter of credit involves several key steps that both the importer and exporter must follow to ensure a smooth transaction. Here’s a step-by-step guide to help you navigate the process:

- Initiation: The importer contacts their bank to request a letter of credit.

- Assessment: The bank assesses the importer’s creditworthiness and determines the terms of the letter of credit.

- Issuance: The bank issues the letter of credit, detailing the specified documents required for payment.

- Verification: The exporter receives the letter of credit and verifies its terms to ensure they are workable.

- Shipment: The exporter ships the goods and prepares the required documents.

- Presentation: The exporter presents the required documents to their bank.

- Verification and Payment: The bank verifies the documents and requests payment from the importer’s bank.

Working with a bank experienced in issuing letters of credit is crucial to ensure a smooth application process. Both exporters and importers should thoroughly understand the terms of the letter of credit and the requirements for payment to avoid any potential issues.

Advantages of a Letter of Credit

A letter of credit offers several significant advantages for both exporters and importers, making it a valuable tool in international trade:

- Reduced Risk: It provides a guarantee of payment to the exporter, significantly reducing the risk of non-payment.

- Increased Security: The secure payment mechanism reduces the risk of fraud or default, offering peace of mind to both parties.

- Improved Cash Flow: Exporters can benefit from improved cash flow as the letter of credit guarantees payment upon presentation of the specified documents.

- Competitive Advantage: Offering a secure payment mechanism can give exporters a competitive edge in the market.

- Flexibility: Letters of credit can be tailored to meet the specific needs of both the exporter and importer, providing a customized trade finance solution.

These advantages make letters of credit a preferred choice for many businesses engaged in international trade transactions.

Disadvantages of a Letter of Credit

While letters of credit offer numerous benefits, they also come with certain disadvantages that businesses should be aware of:

- Cost: The fees associated with letters of credit can be significant, ranging from 0.5% to 2% of the total credit being backed.

- Complexity: Setting up and managing a letter of credit can be complex, requiring specialized knowledge and expertise.

- Risk of Discrepancy: There is always a risk of discrepancies between the letter of credit and the sales agreement, which can lead to delays or disputes.

- Limited Flexibility: Once established, a letter of credit can be inflexible, making it challenging to make changes to the terms of the agreement.

Understanding these potential downsides is crucial for businesses to make informed decisions about using letters of credit in their trade finance strategies.es to make informed decisions about using letters of credit in their trade finance strategies.

Managing Risk with a Letter of Credit

A letter of credit can be an effective tool for managing risk in international trade transactions, especially for non existing trade customers (i.e. new customers that you may not trust yet). By providing a guarantee of payment, it helps reduce the risk of non-payment and improves cash flow for exporters.

However, it’s essential to understand the associated risks and take steps to mitigate them. Here are some strategies for managing risk with a letter of credit:

- Review Terms Carefully: Ensure that the terms of the letter of credit align with the sales agreement to avoid any discrepancies.

- Ensure Document Accuracy: Make sure that the specified documents required for payment are accurate and complete.

- Work with Experienced Banks: Partner with banks that have experience and a track record in issuing letters of credit to ensure a smooth process.

- Monitor the Letter of Credit: Regularly monitor the letter of credit to ensure it is being used correctly and that payments are made on time.

By understanding the benefits and risks of a letter of credit and taking proactive steps to manage those risks, exporters and importers can use this trade finance solution to enhance their international trade transactions.

Letters Of Credit – A Way to Make Money Without Money?

A transferable letters of credit in international trade, enables the seller (or beneficiary) to buy products to fulfill the sales contract from a third party without using their own funds, instead using the funds from the contract itself.

Think of it as an advance on the payment (opposed to a guarantee on non payment) that will be received on completion of the contract. Once this “mother” letter of credit has been born, it can be split up and transferred to as many parties as needed as long as the total does not exceed the amount of the original “mother” letter of credit.

Credit terms encompass the specific terms and conditions under which a bank commits to make payment to a seller on behalf of a buyer, contingent on compliance with the stipulated documentation.

Transferable letters of credit are often successfully used to purchase high value goods without having to dip into company funds where cash flow may be tight and the company may not be sitting on bundles of cash and need to receive payment before delivery of the goods or project.

Be warned however, they are not as simple to obtain and use as some would like you to believe. It certainly should not be considered a way to make money, without money.

Standby Letters Of Credit

There is one other type which is not actually meant to be used, which is known as a standby letter of credit.

This is a last resort or safety net for the seller reducing the financial risk within the contract. It’s basically a guarantee of the payment from the issuing bank on the behalf of the seller.

If the buyers business for some reason was to declare bankruptcy or was just unable to make the payment, this would make the confirming bank pay but the intention is that it will never need to be used.

This letter of credit is usually issued in good faith providing proof that the buyer’s credit is in good standing with the issuing bank and that they will be able to make the payment without any issues.

The buyers company will undergo a credit check before the issuing bank releases the letter of credit giving security that the company is stable and not under any financial trouble.

UCP 600

Something else to be aware of relating to letters of credit is that there have been a set of rules created and agreed by the International Chamber of Commerce, known as the Uniform Customs and Practice for Documentary Credits (commonly called “UCP”), which banks and financial institutions that issue letters of credit are subject to.

This is a subject on its own so we won’t go into detail here but it’s certainly something you must be aware of. See our video below for details on UCP 600 to get you started:

A Letter of Credit Example

Using such a case of a real world example, we can hopefully show you more clearly the process and just how letters of credit work.

Letters of credit are important in trade transactions due to their secure nature. Professional preparation is essential to avoid costly errors and delays.

Not so long ago we were asked to work with a small London based building company who had been awarded a nicely sized contract to build a brand new, modern sports facility in the United Arab Emirates.

The high end sports facility would include a swimming pool, saunas in the changing rooms, two basketball courts, a full size gym with aerobic equipment as well as a lounge area complete with table tennis and pool tables and health bar.

As you can imagine, this type of facility doesn’t come cheap and the contract value was negotiated and agreed at just over £1.6 million (GBP). This included the raw materials, exporting of the required materials that could not be sourced within the UAE and the construction of the facility.

How To Raise £1.6m

As you can probably imagine, most businesses don’t have £1.6m sitting in their company bank account so raising the funds to complete the project was something that needed to be handled. This company took the traditional avenue and approached their bank for finance but for one reason or another weren’t granted the entire amount. They subsequently approached other finance companies who offered them funds but the terms of repayment weren’t suitable. At this point, the project looked to be in jeopardy and the contract had to be reconsidered.

To embed this infographic, copy and paste the code below:

Unworkable Letter Of Credit Explained

Almost half of the letters of credit received in the UK are unworkable according to some research, the buyer requests documents which the seller may be unable to produce, so be aware and be proactive, not reactive.

As you can see, knowing how to use letters of credit are a great way to fulfill projects when cash is tight but it’s really important to know what you’re doing as they can be complicated and you must be aware of the types of letters of credit for use.

If you get it wrong, you could be left holding the can and unfortunately there are many horror stories of contracts going desperately wrong due to people not understanding how to properly establish and use letters of credit.

Don’t be one of them and get the right letter of credit training!

ABTS® International Trade Mastery Programme

Understand exactly what is a letter of credit and learn how to use letters of credit by enrolling in our online course. Our course streamlines what you’ll need to know to be successful using letters of credit with real-world knowledge.

Taught by Alan Bracken, with 40+ years of commercial experience in logistics, he skips all the theory you’ll never need to know but teaches you the practical side of how to use a letter of credit.

For more details see our letter of credit course syllabus.

Check out our reviews on TrustPilot to see just how our courses have benefited our students.